Mission Valley Flood Insurance & NFIP Requirements: How FEMA’s CRS Rating and New Flood Maps Impact Apartment NOI

By Scott Engle (Broker DRE #01332676 | Corp DRE #02075336) — California Property-Management Broker, San Diego County

Last Updated: March 2, 2026

Introduction

Mission Valley apartments sit within the mapped San Diego River floodplain, making flood insurance a structural financial variable—not an optional add-on. FEMA map classifications, National Flood Insurance Program (NFIP) participation, lender requirements, and California disclosure statutes directly affect NOI, underwriting, and asset value. In this corridor, flood risk is measurable, regulated, and enforceable.

TL;DR

- Mission Valley is geographically exposed due to the San Diego River floodplain.

- San Diego participates in the NFIP and holds a Class 7 CRS rating, granting a 15% premium discount.

- FEMA Physical Map Revisions (PMR) effective March 3, 2026, can reclassify properties into mandatory coverage zones.

- California Government Code § 8589.45 requires flood hazard disclosure in all residential leases.

- Flood insurance compliance functions as capital preservation, preventing Cap-Rate Compression.

Quick Answers Box

Why is Mission Valley structurally flood-prone?

It lies within the San Diego River floodplain, where elevation and overflow history create measurable exposure monitored by the USGS Fashion Valley Mall stream gauge.

What does San Diego’s CRS Class 7 rating mean?

It grants policyholders a 15% premium discount, reflecting municipal compliance with FEMA’s floodplain management standards as of 2026.

When is flood insurance legally mandatory?

Coverage is mandatory for properties in a Special Flood Hazard Area (SFHA) with federally regulated financing.

What legal disclosure applies to Mission Valley landlords?

Under GC § 8589.45, landlords must disclose in writing if a property sits in a flood hazard zone.

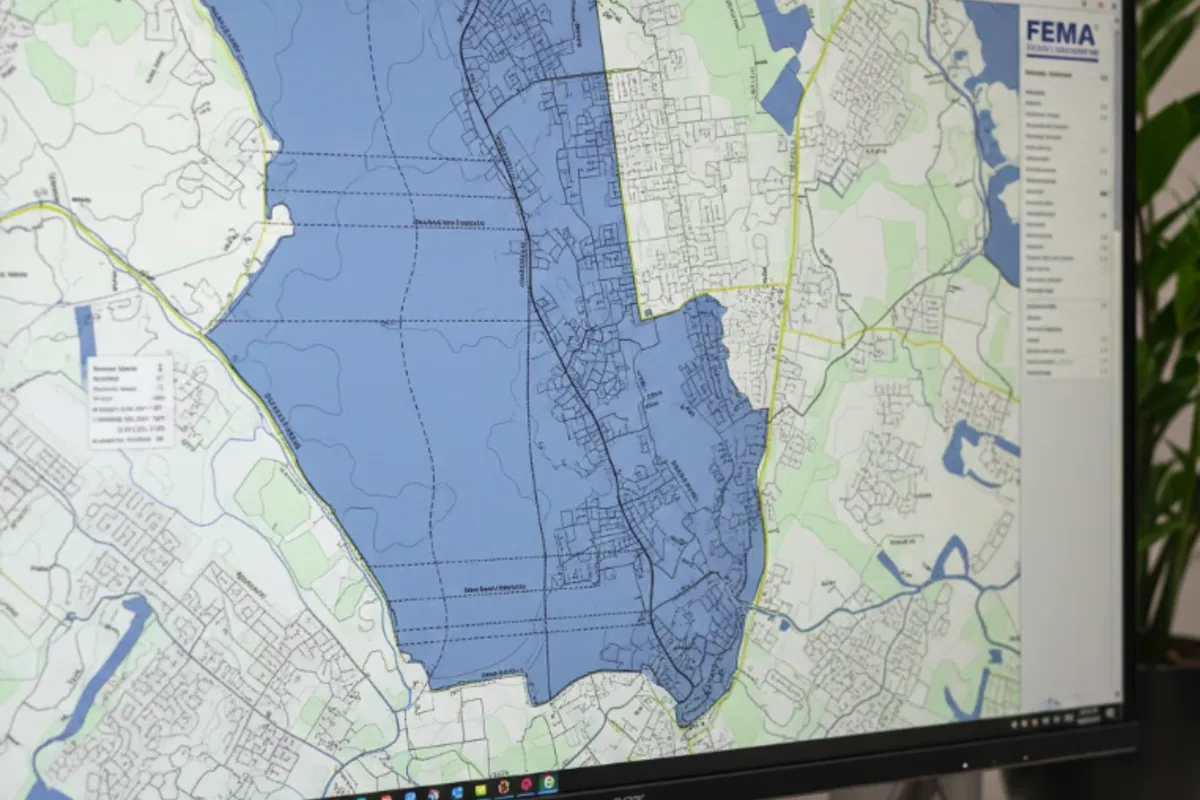

Why Mission Valley Is Geographically Exposed

Mission Valley’s location within the San Diego River corridor places large portions of its housing stock inside FEMA-mapped flood zones. The valley’s low elevation relative to surrounding mesas creates concentrated overflow risk. FEMA flood modeling for these parcels relies heavily on elevation data tied to river channelization projects completed after the 1980s flood events.

Subterranean parking common in podium-style developments increases structural vulnerability.

NFIP policies often treat below-grade parking differently from elevated living space, limiting coverage scope. Owners seeking Mission Valley property management must audit their Elevation Certificates (EC) to ensure accurate premium rating. This verification is a key component of a high-performance Maintenance Arbitrage strategy.

How NFIP Participation and CRS Class 7 Reduce Premiums

San Diego’s participation in the NFIP and its Class 7 CRS rating reduce policyholder premiums by 15 percent. This rating rewards municipalities for proactive floodplain management. However, if a property lies in an SFHA with federally backed financing, flood insurance remains a non-negotiable lender compliance requirement.

How FEMA Map Revisions Change Insurance Requirements

FEMA Physical Map Revisions (PMR), specifically the update taking effect March 3, 2026, and Letters of Map Revision (LOMR / LOMR-F) can change whether flood insurance is required. Properties may shift into higher-risk designations following updated Base Flood Elevation (BFE) modeling. Failure to monitor these updates can result in lender-imposed Force-Placed Insurance at substantially higher premiums, directly attacking your NOI.

California Disclosure and Security Deposit Implications

Landlords must disclose flood hazard status under Government Code § 8589.45. Failure to disclose exposes owners to civil liability. Furthermore, if a unit becomes uninhabitable due to flood damage, Civil Code § 1950.5 governs the handling of security deposits. Improper withholding following a force majeure event increases liability beyond physical loss.

Advanced Financial Modeling: Maintenance Arbitrage

Proactive compliance increases asset value by avoiding predatory force-placed rates. Maintenance Arbitrage logic proves that insurance is an investment in capital preservation.

- NFIP Premium: $2,500 annually

- Force-Placed Scenario: $8,000 annually

- Annual Savings: $5,500

At a 5.2% cap rate, avoiding force placement preserves: $5,500 ÷ 0.052 = $105,769 in asset value.

Flood Loss Scenario Modeling

| Scenario | Financial Impact |

|---|---|

| Annual NFIP Premium | $2,500 |

| One-Month Rent Interruption (20 units @ $2,800) | $56,000 |

| Structural Damage Event | $50,000–$250,000 |

| Combined Loss Exposure | $100,000+ |

Diagnostic Audit Checklist - Mission Valley Ready

- ☐ Elevation Certificate (EC) verification on file

- ☐ LOMR-F status confirmed for podium structures

- ☐ HVAC and electrical panels elevated at least 1ft above BFE

- ☐ Private Loss-of-Rent endorsement secured

- ☐ Annual FEMA PMR monitoring process in place

Binary Contrast: Insured Compliance vs Uninsured Exposure

| Insured Compliance | Uninsured Exposure |

|---|---|

| Predictable annual premium | Force-placed premium spikes |

| CRS discount applied (15%) | Rental income interruption |

| Stabilized NOI | Cap-rate compression |

Summary

In the San Diego River corridor, Maintenance Arbitrage is about navigating the delta between FEMA’s Base Flood Elevation and a property’s specific features. For assets in Mission Valley property management portfolios, the 15% CRS discount is a baseline. True protection comes from aligning Elevation Certificates with private-market loss-of-rent endorsements that the NFIP traditionally excludes.

About the Author

Scott Engle is the Broker/Owner of Realty Management Group. Licensed in California since 2002, Scott oversees a portfolio exceeding 1,000 transactions. He integrates floodplain compliance and asset-level NOI modeling for high-density corridors across San Diego County, including Chula Vista and El Cajon.